Our Publications

Advanced Information System (AIS)

Success Journey Report

3 Key Areas:

From the inception of 4G through 5G, has applied the strategy of rapid deployment of network.

The consumer business, what leads to the current pricing.

Enterprise business, what is the strategy and logic behind it.

Key Findings

AIS will continue to be a revered consumer brand as it adopts innovative services based on advanced fixed and a mobile 5G platform.

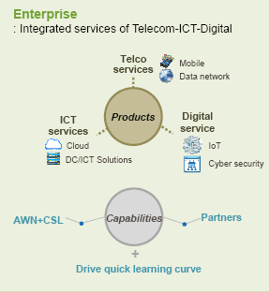

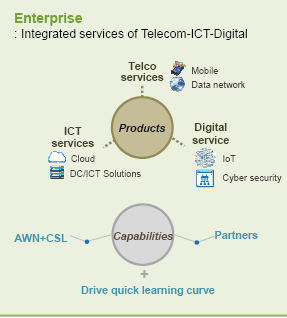

AIS is positioning itself to become the go-to 5G enterprise/industrial provider.

AIS has built a solid data center network with disaster recovery and redundancy split across four regions nationwide.

Mobile ARPU growth will be challenging but a duopoly market might reduce pressure from 2024 to buy market share with freebies.

Fixed broadband and enterprise business will help to buoy the revenue equation at AIS by capturing the pent-up demand for broadband (and content).

FBB provides a platform from which AIS will grow its digital content services business, but we expect AIS to take a conservative approach in terms of content acquisition costs.

Consumer 5G business strategy is cautiously conservative for the time being.

AIS's balance sheet and cash flow should be able to support levels of CAPEX spending on the order of Baht 28-30+ billion per year out to 2027E.

Enterprise 5G business strategy holds promise for AIS, as AIS is starting from a relatively small presence in the enterprise market.

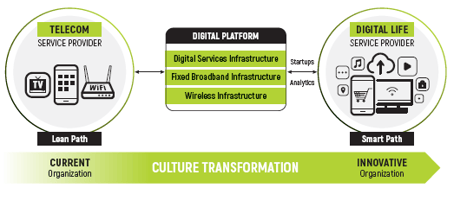

AIS's DX Strategy

1) Organic Growth was going to be too slow, so AIS has expanded and filled in gaps through key acquisitions in fixed broadband and IPTV

2) Accelerating the brand as the go-to provider for digital life services

3) Construct Digital Services on a 5G + Fixed Broadband platform

4) Continue to keep Customer Experience at the center of the GTM strategy

5) Personalize and drive CX with Cloud + AI based Omnichannel

6) Counter inflationary pressures by reducing costs with AIOps and Automation

7) Making Cyber Security a pillar of the AIS brand

8) Be the Market Leader for Sustainability / Energy Savings

Key Takeaways

Financial and Operational Analysis

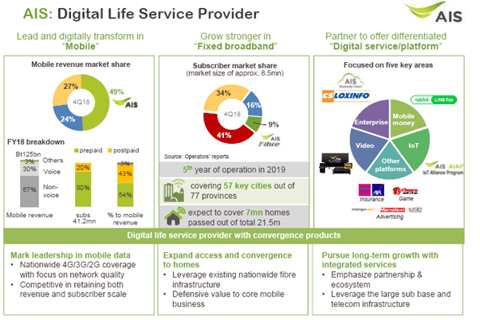

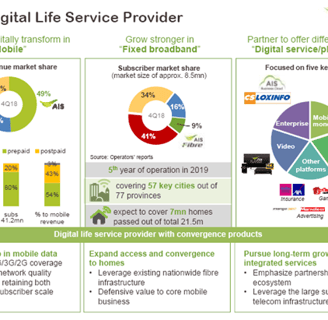

Revenue growth for AIS is expected to come from various sources, including 5G consumer services, 5G enterprise services, fixed enterprise services, fixed broadband, cloud connectivity, and co-location services. However, the fixed broadband sector may plateau due to the acquisition of 3BB, requiring network integration. AIS is actively promoting 5G adoption by offering discounts to migrate 4G post-paid customers to 5G. Thoth Advisory predicts that 5G's share of AIS's mobile subscribers will increase from 15% in 2022 to 39% in 2027.

1

AIS's EBITDA faced challenges in 3Q22 and 4Q22, with YoY declines due to increased marketing spending, rising utility costs, and growing maintenance expenses as the 5G network expands. Content costs are also expected to rise as AIS expands its digital services. The regulatory fee paid to the government remains at 4.2% of core service revenue.

2

Network operating expenses (OPEX) are on the rise, primarily due to increasing electricity costs and the greater power demand from 5G base stations. In 3Q22, network costs grew by 10.9% YoY, and AIS is closely managing this line item.

3

AIS sees a revenue opportunity in 5G enterprise services, which is forecasted to contribute 3.2% of Core Service revenue by 2027. To capitalize on this, AIS is investing in network slicing, cloud computing, and Multi-access Edge (MEC) to offer a single platform to enterprise customers. The introduction of NR Standalone positions AIS well for private networking and network slicing for enterprises.

4

AIS's capital structure and balance sheet appear stable and capable of supporting annual CAPEX expenditures of approximately Baht 30 billion, barring any unexpected extraordinary expenses.

5

The impending TRUE/DTAC merger may reduce pricing pressure and Average Revenue Per User (ARPU). However, GlobalData believes that both post-paid and pre-paid ARPU are on a declining trend that is difficult to reverse. Pre-paid ARPU is particularly vulnerable to inflationary pressures. The intense competition in the market, including the sale of unlimited post-paid data packages, has driven ARPU downward in recent years. The reopening of borders is expected to boost mobile revenues in 2023.

6

AIS Success Journey Report

1) Executive Summary

2) AIS Digital Transformation Journey

3) Financial and Operational Analysis

4) Consumer Strategy

5) Enterprise Strategy

6) Network Modernization